Something to Consider…

We previously asked church leaders about the following situation:

During the Great Recession of 2008 some churches decided to freeze staff pay. Perhaps giving at your church has improved lately—reflecting an improving economy. Your staff senses that a pay increase could be in the works.

How do you determine appropriate compensation?

While the Bible warns of the wages of sin

in a spiritual sense, it also speaks in a more material sense about a worker’s wages. As one can see from some of the verses offered here, the two sometimes even intersect:

Do not muzzle an ox while it is treading out the grain.

Deuteronomy 25:4Pay them their wages each day before sunset, because they are poor and are counting on it. Otherwise they may cry to the Lord against you, and you will be guilty of sin.

Deuteronomy 24:15So I will come to put you on trial. I will be quick to testify…against those who defraud laborers of their wages…but do not fear me,

says the LORD Almighty.

Malachi 3:5Stay there, eating and drinking whatever they give you, for the worker deserves his wages."

Luke 10:7Who serves as a soldier at his own expense? Who plants a vineyard and does not eat its grapes? Who tends a flock and does not drink the milk?

1 Corinthians 9:7Look! The wages you failed to pay the workers who mowed your fields are crying out against you.

James 5:4

…because whoever plows and threshes should be able to do so in the hope of sharing in the harvest. If we have sown spiritual seed among you, is it too much if we reap a material harvest from you? If others have this right of support from you, shouldn’t we have it all the more?

1 Corinthians 9:10-12

Church leaders who are entrusted with setting compensation for their paid staff should understand that church employees should be paid appropriately. This means paying someone commensurate with the responsibilities that they have been assigned and the expected level of educational attainment.

Church leaders who are entrusted with setting compensation for their paid staff should understand that church employees should be paid appropriately. This means paying someone commensurate with the responsibilities that they have been assigned and the expected level of educational attainment.

Sadly at some churches leaders try to get off by paying their staff as little as possible. Perhaps they console themselves that an employee will receive their reward in heaven or that the church can’t afford to pay them a greater amount.

Statistics, unfortunately, don’t paint a picture of Christians being very generous. The average amount of income that Christians give to their church is only around three percent. Some denominations are a tiny bit higher while others are tiny bit lower. Either way we’ll venture to suggest, they give considerably below where the bar was set for the tithe in the Old Testament. Perhaps those churches who cannot afford to pay their staff appropriately should first ask their members if they are supporting their church in a God-honoring way.

So how does a church that wishes to support its staff in a God-honoring way go about determining whether pay is reasonable

or not? One approach is to contact at least three other churches of similar size within your church’s geographic region and ask them to share with you compensation data for their paid staff. While this sample size would be considered small, if documented properly it should be enough to satisfy an IRS inquiry.

But what if other churches won’t share their information or you can’t locate other churches similar in size to yours? After all, we are dealing with what many consider to be a private matter. An alternative would be to utilize one of the salary surveys available to church leaders.

If your church is part of a denomination, your denomination may already have a salary survey that you can refer to. But even if your church is not part of a denomination that produces a salary survey, there are other reputable surveys available for a nominal cost. Generally these surveys collect data from many churches from all over the country and across denominations. The data may be organized and published in book form annually or they may be available online. If survey results are online, it most likely will be getting revised on an ongoing basis as churches add or update their compensation information or as a churche’s data is deleted because it’s no longer up to date.

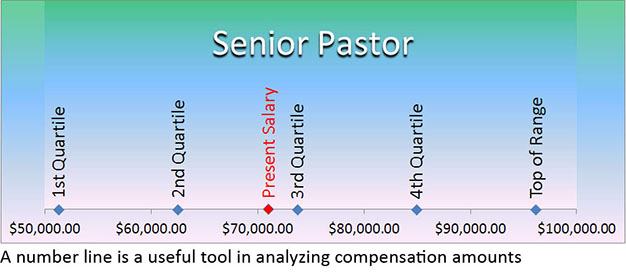

Even more helpful would be going to the trouble to create a number line and putting the proposed salary for a position on it.

Nevertheless it’s unlikely that your situation will line up perfectly with that found in a compensation survey. For example, does your senior pastor have 13 years of experience and is ordained like the survey lists? So how do your compensate for variables? We suggest that for each paid position at your church that you come up with a salary range. The good news is that it’s not as hard as it may sound.

Two reputable surveys that we are familiar with display data with at least four data points, average (or mean), median (half the raw data is higher and half is lower), 25th percentile (25 percent of the raw data is lower), or 75th percentile (25 percent of the raw data is higher). Survey data may also be organized by geographical region, attendance, years of service, annual church budget or other categories. We suggest that if multiple categories are available pick two or three that make the most sense for your congregation. For example, when you recruit for a position and you search nation-wide, using data from a particular geographic area may not make as much sense as your attendance range would.

Take the number in the mean or average column or row from the two or three categories that you’ve chosen and average them. If you only can choose data from various ranges of annual church budgets, that will do as well.

Next take the average that you’ve either calculated or chosen and multiply it first by 0.8 and then by 1.5. If you are getting the idea that perhaps some skill with a spreadsheet like Microsoft Excel would be helpful, you’re right. You now have the bottom and top of a workable salary range. If you’re really ambitious you can also calculate three equally spaced intermediate points and display all your calculations graphically on a number line.

Having a high and low number for each position based on real data is quite helpful in determining whether or not your church is paying each employee appropriately. Even more helpful would be going to the trouble to create a number line and putting the proposed salary for a position on it. (See our illustration above.) Compensation for staff members with more experience than their colleagues at other churches should trend towards the higher end of the salary range. The opposite applies to employees with less experience than their colleagues at other churches.

If you would like help in putting together a number line that graphically shows a salary range for each paid position at your church, we can do that for you at a reasonable cost.

Benefits

So far we’ve only visited the issue of calculating appropriate pay. No discussion of compensation packages would be considered complete if we didn’t include self-employment tax reimbursement for ordained staff, retirement plans, health plans, insurance plans, or reimbursement of business expenses.

If business expenses are reimbursed to your paid staff under an Accountable Reimbursement Plan, the IRS considers such payments as non-taxable to the employee. If your church doesn’t have such a plan, those payments are considered taxable income. It used to be that employees could deduct a portion of their unreimbursed employee business expenses on their federal income tax form. But as of January 2018 that deduction is no longer available due to new tax law passed in 2017. Contact us if you need an Accountable Reimbursement Plan. While we’re on the topic of reimbursing business expenses, please understand that the IRS requires that these reimbursements be in addition to an employee’s compensation. For example, let’s say that a pastor visits several different hospitals over the course of a year and at the federal mileage rate would be eligible to received $3,000 next year in reimbursements for business miles driven. The church could not legally allocate $3,000 of his or her budgeted salary for mileage. Instead it must reimburse mileage and other expenses in addition to his or her budgeted salary.

While regular employees’ withholding for Social Security and income taxes is handled much like for any other business and is relatively straightforward, it’s less so for ordained staff members. The IRS considers ordained clergy to be employees for income tax purposes but self-employed for Social Security taxes. While an employer pays one half of an employee’s Social Security taxes and the employee pays the remaining half, a self-employed person has to pay both halves. But like they say on those late-night TV ads—there’s more! Some ordained clergy have legally opted out of participating in Social Security altogether. For those folks, neither they nor their churches pay any Social Security taxes on their behalf.

However, for those ordained staff members who have not opted out of Social Security, some churches go ahead and add to their pay an amount that would be equivalent to the portion of total Social Security taxes the church would otherwise be obligated to pay. While we would consider this a very considerate thing to do, please understand that this additional amount would be considered by the IRS as taxable income to the employee.

When a church overpays its staff, most notably its lead pastor, this is as much of a problem as underpaying staff, perhaps worse.

Briefly, regarding insurance and retirement programs, these can get complicated so we recommend that you contact a qualified broker who is familiar with working with churches. They can inform you about any limits that you have to abide by in order to keep policies from becoming taxable to the employee and about options that would benefit your staff the most at the lowest possible cost to the church. For example, employers can provide their employees with up to $50,000 in term life insurance coverage as a non-taxable benefit. As soon as that coverage goes over $50,000 it becomes taxable. Brokers can help church leaders consider other type of insurance coverage such as medical, dental, disability and vision.

As for retirement plans, churches are allowed to participate in plans that don’t meet the requirements of the federal Employee Retirement Income Security Act or ERISA. Be sure that your broker can explain the advantages and disadvantages of participating in either an ERISA or non-ERISA plan. To our knowledge there are only two companies who offer non-ERISA retirement plans to churches.

You may be curious why we haven’t mentioned housing allowance for ordained staff. Mostly that is because we already have another article available that deals specifically with that topic. If you CLICK HERE you will be taken to it. Nevertheless, the short answer is that the amount of salary that is designated as housing allowance is a portion of the money already budgeted for compensation. Raising or lowering it makes no difference to the church’s finances. Setting it too low, however, can deprive a qualified ordained employee of tax savings that he or she is entitled to.

When Too Much Is A Problem

While many churches struggle to pay their employees appropriately, some churches try to compensate their senior pastor as extravagantly as possible. When a church overpays its staff, most notably its lead pastor, this is as much of a problem as underpaying staff, perhaps worse. The Internal Revenue Service expects that persons in positions of control, such as a senior pastor, receive compensation that is considered reasonable.

Failure to keep an individual’s total compensation reasonable

can result in excise taxes being assessed on not only the employee in question, but on the board members who authorized the excessive pay, too. Please understand that the IRS’ perspective on total compensation extends beyond salary. It also includes benefits as well. Even if a senior pastor’s salary is reasonable, but he or she receives an extremely generous package of benefits, it could be considered excessive and as a result could result in excise taxes being due.

Paying church employees appropriately is not only an obligation placed on church leaders by scripture, but also by the Internal Revenue Service by law. If you would like help in determining whether your church is compensating its employees in a God-honoring and legal way, please call us. We’re here to help you be a beacon of integrity to your community.

Please Note: This information is provided with the understanding that Church Administrative Professionals is not rendering professional advice or service.

Have an idea for a situation that you would like us to include on this page OR

Prefer to receive our periodic "In Pursuit of Excellence" analysis as an e-mail instead of as a postcard? Click Here

![]() © 2015 Church Administrative Professionals LLC

© 2015 Church Administrative Professionals LLC

All rights reserved

Tel: 913.424.5959 / 816.507.7895